February/March 2024 Kontos Kommentary

The following commentary is produced by Tom Kontos, Chief Economist, ADESA Auctions.

Spring appears to have sprung in the wholesale market, as average prices jumped another four percent month-over-month in February and have continued to rise significantly in March. Retail used vehicle and CPO sales also showed February increases.

Wholesale Market Trends*

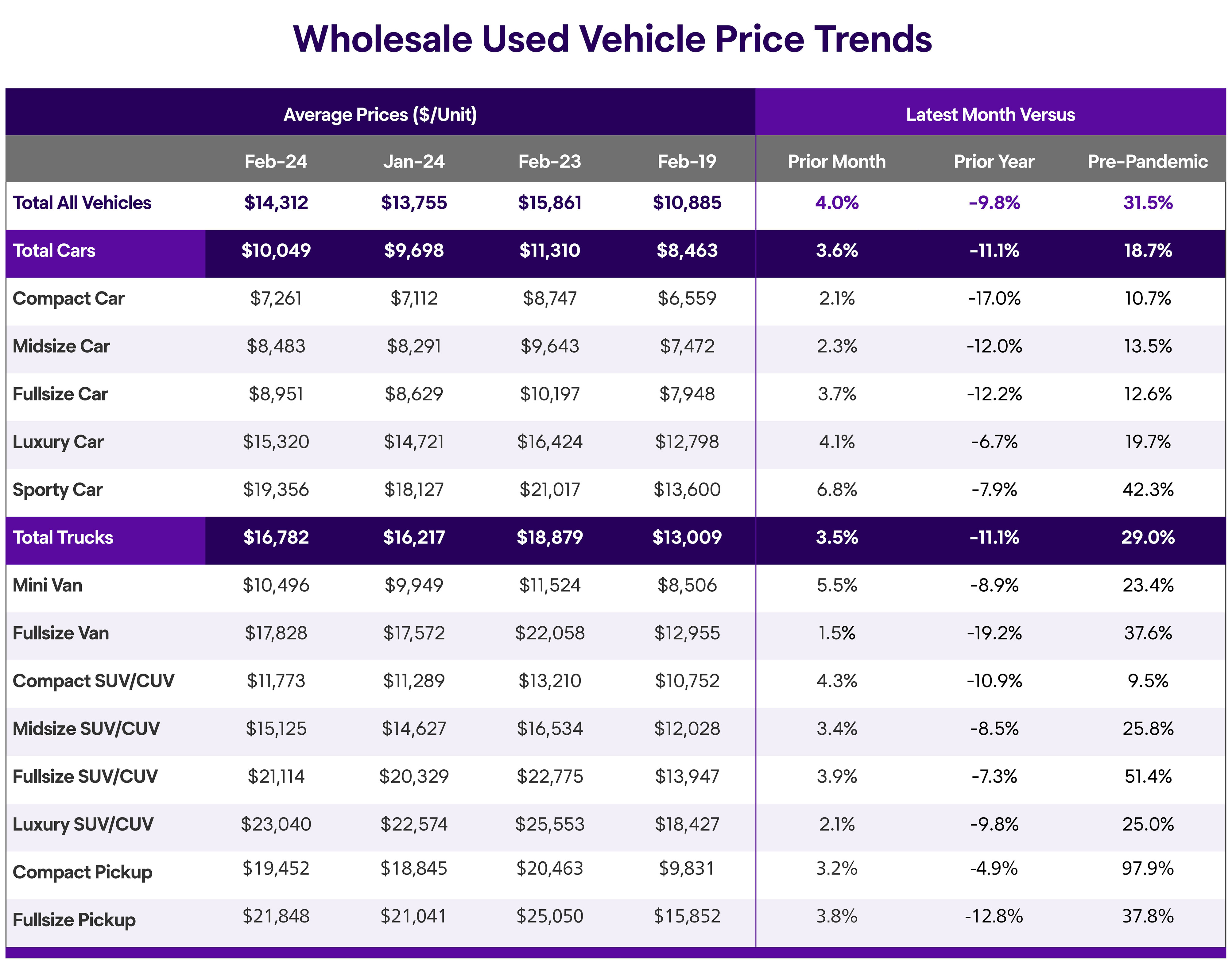

According to ADESA US Analytical Services’ monthly analysis of auction industry used vehicle prices by vehicle model class, wholesale prices in February averaged $14,312—up 4.0% compared to January, down 9.8% relative to February 2023, and up 31.5% versus pre-pandemic/February 2019, as shown below.

All model class segments showed month-over-month increases. Average prices have continued to rise so far in March and stood at $14,536 for the week ending March 17.

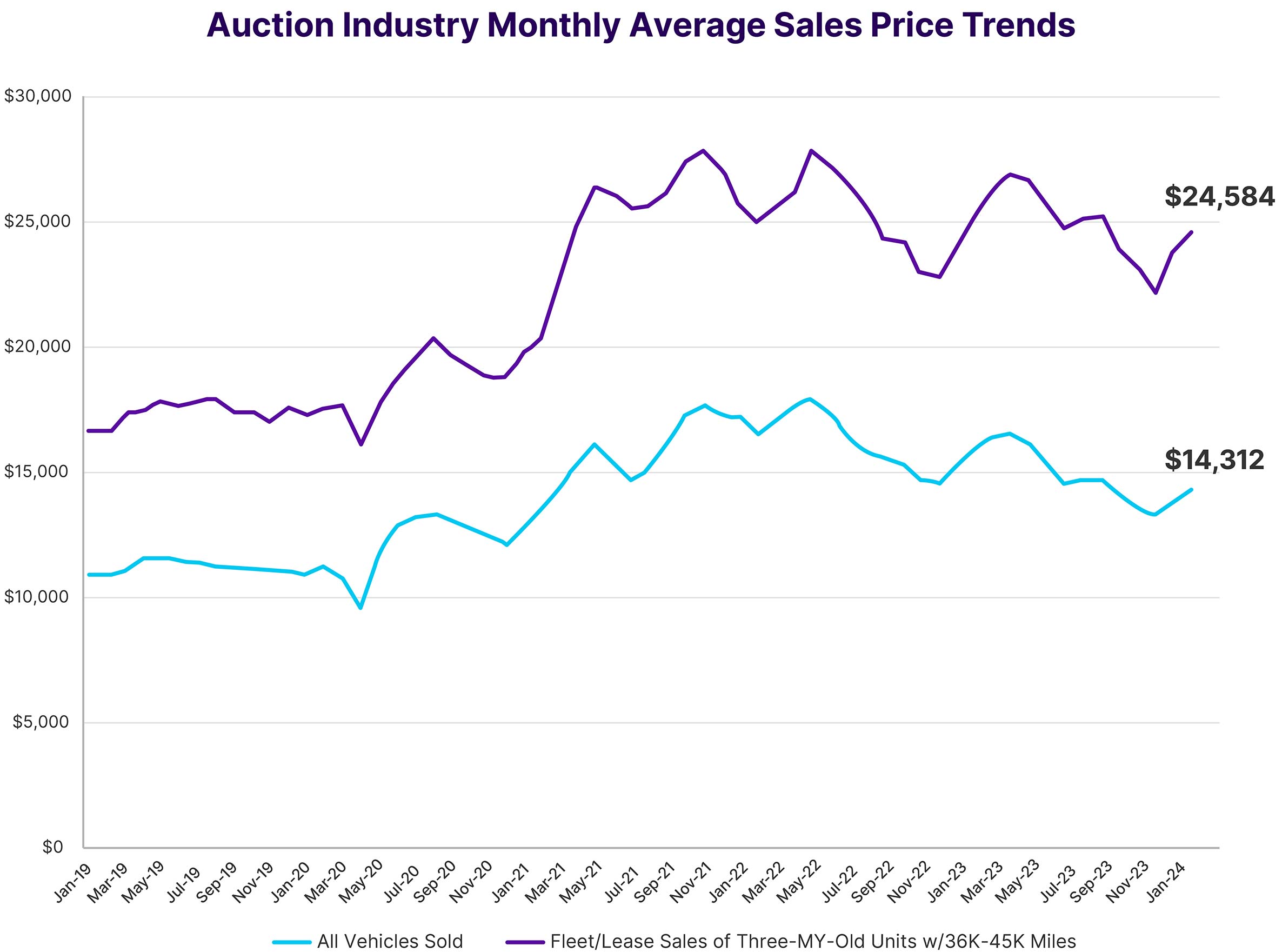

Further insights on wholesale price trends can be gained by holding constant for auction sale type, model-year age and mileage (the upper line in the following graph, which represents “Late-Model” units), as well as price trends for all vehicles sold (the lower line in the graph below).

As the graph shows, average prices for “Late-Model” used vehicles as defined here have risen faster than overall prices so far this year. Average prices for these late-model vehicles have continued to rise in March and stood at $25,348 for the week ending March 17. These rapid price rises are indicative of interest by consumers, and therefore dealers, in more-affordable substitutes for high-priced new vehicles.

A spreadsheet with historical data broken out by model class for the table and graph in this section has been provided with this report for your convenience in tracking these trends.

Retail Market Trends

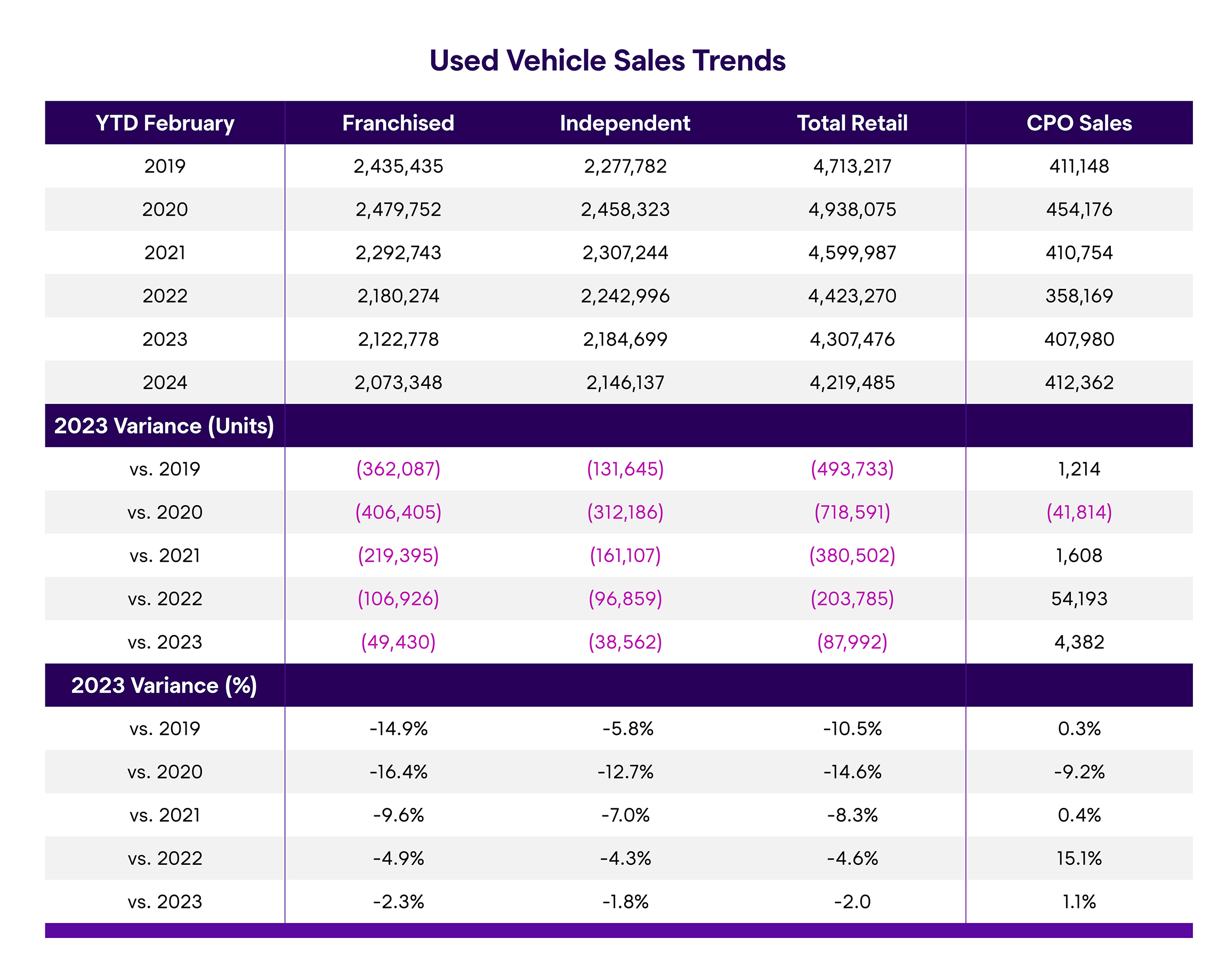

The following graph and table summarize ADESA US Analytical Services’ analysis of NADA and Motor Intelligence data, respectively, on retail used vehicle and certified pre-owned (CPO) sales in February.

As the figures show, overall retail used vehicle sales are off to a slower start than any of the previous five years, despite a modest year-on-year rise in February. On the other hand, year-to-date CPO sales are up even when compared to pre-pandemic levels. This is once again indicative of consumer interest in more-affordable substitutes to expensive new vehicles.

#Trendspotter

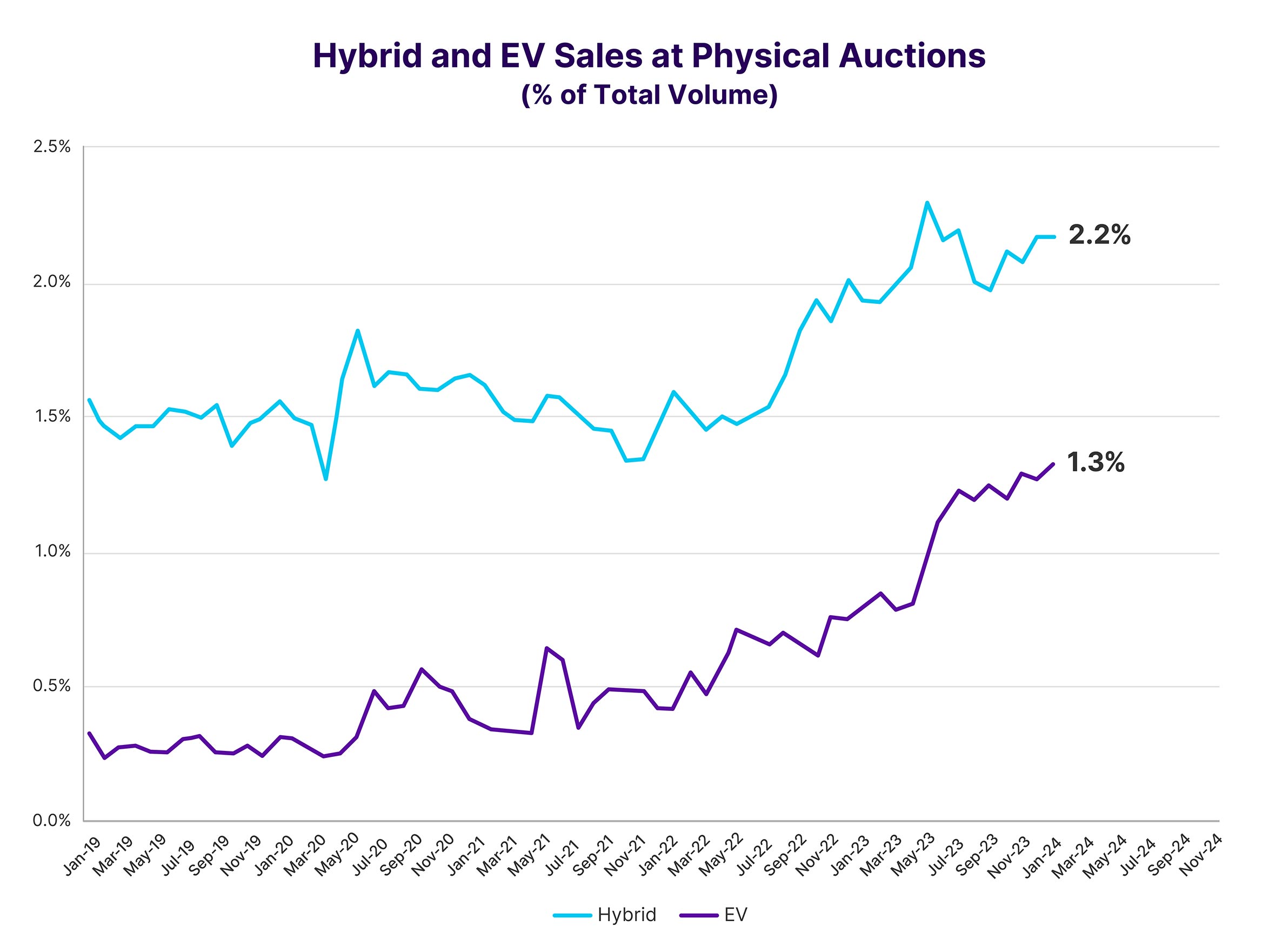

Recently, a lot of ink has been spilled not only on EVs, but increasingly on Hybrid vehicles. I thought it timely, therefore, to share a couple of graphs I’ve developed to monitor auction price and volume trends for these alternative fuel vehicle types. The first graph shows that both these vehicle types still represent a small percentage of total auction sales, but that share is growing. These volume trends tend to lag new-vehicle sales trends by a few years, so it will be interesting to see how these patterns may change over time.

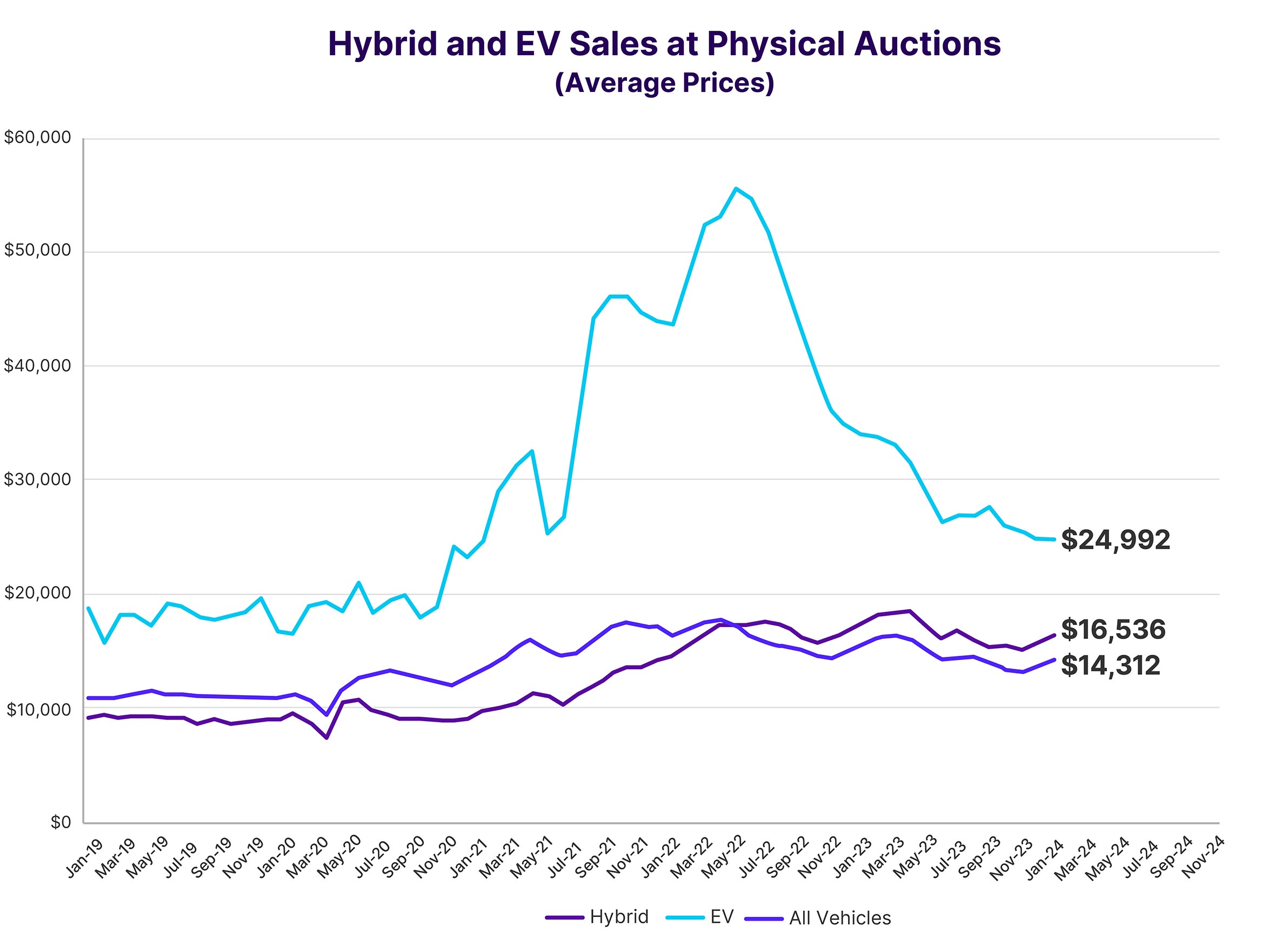

The second graph shows average auction prices for the two vehicle types, along with the same total auction average prices shown earlier in this report. The EV line displays the same general return towards market price trends that I described for the Tesla Model 3 in my December and January Kontos Kommentary #Trendspotter. Average Hybrid vehicle prices, however, have gone from being below-market to above market, although this could perhaps be partially due to changes in model mix.

I will continue to monitor these trends going forward. I hope you find this information useful, and I welcome your feedback.