Top 10 Trends from the Mitchell 2016 P&C Conference

At the 2016 Mitchell Property and Casualty Conference, keynotes, breakouts and everything in between were focused on technology and social trends that are changing the way we interact with one another and do business. From augmented reality to information security, here are 10 of the many trends that were top of mind at the conference.

Virtual and Augmented Reality Are Literally Showing Us the Way

This summer’s Pokémon Go craze reminded us that augmented reality can be really engaging and fun—but it also has incredible practical applications for the P&C and collision repair industries. For instance, Los Angeles-based Daqri makes a smart helmet that projects information to guide the wearer through complex repair scenarios. Technology like this could be a boon to auto insurers and collision repairers looking to ensure increasingly complex repairs are done correctly. It could also help prevent injuries in high-risk jobs, ultimately reducing workers’ compensation claims. Meanwhile, at Cedars Sinai Medical Center, a trial is underway that uses inexpensive virtual reality headsets to ease patient pain. Early results suggest an average 24 percent decrease—similar to the pain reduction they see when administering narcotics.

Consumer Self Service Is the Way of the Future

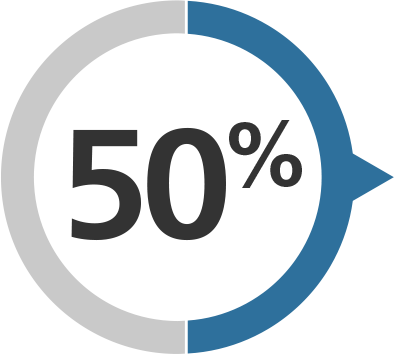

Driven by the ubiquity of mobile devices and a growing preference among consumers, particularly Gen Y and Gen Xers, to communicate exclusively through digital self-service, Mitchell believes that consumer self-service interactions will grow from five percent today to 20 percent by 2020.

Mitchell believes consumer self-service interactions will grow from five percent today to 20 percent by 2020.

Since a positive first notice of loss (FNOL) experience is a the second largest contributor to customer satisfaction—only settlement has a greater influence—insurers seeking to tap into this growing audience would do well to invest in technology that facilitates this process.  Further, when FNOL is submitted via a mobile app and incorporates images, cycle time is significantly reduced. An expeditious claims resolution process benefits both insurance companies, with less hands-on case-management time, and the insured, with a more user-friendly process.

Further, when FNOL is submitted via a mobile app and incorporates images, cycle time is significantly reduced. An expeditious claims resolution process benefits both insurance companies, with less hands-on case-management time, and the insured, with a more user-friendly process.

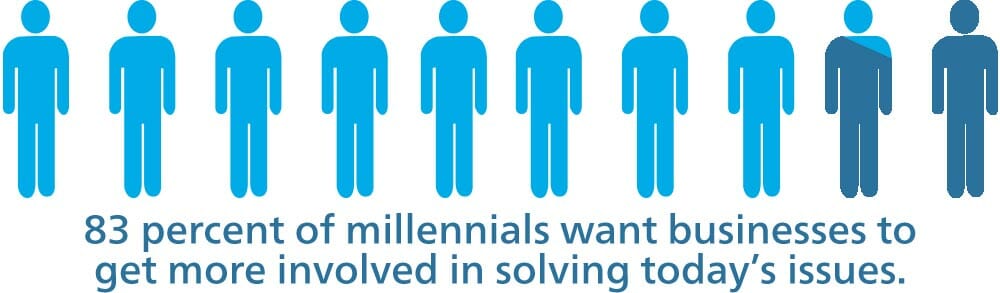

Human Leadership is the Future of Business

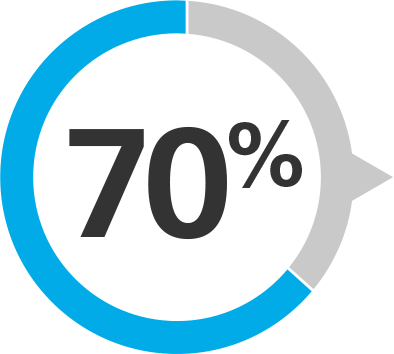

In his keynote address, Soft Power: The Software Engineering Humanity into Leadership, social strategist John Gerzema spoke about how people—millennials in particular—are seeking human business leadership in which companies get more involved in solving today’s issues. In fact, 72 percent of them would take a $7,600 pay cut to work for a company with a culture and values they admire. Why does this matter to the P&C industry? According to Gerzema, insurers can build trust with this important buying group by using AI interfaces and automating processes to reduce transaction time and claims costs.

In his keynote address, Soft Power: The Software Engineering Humanity into Leadership, social strategist John Gerzema spoke about how people—millennials in particular—are seeking human business leadership in which companies get more involved in solving today’s issues. In fact, 72 percent of them would take a $7,600 pay cut to work for a company with a culture and values they admire. Why does this matter to the P&C industry? According to Gerzema, insurers can build trust with this important buying group by using AI interfaces and automating processes to reduce transaction time and claims costs.

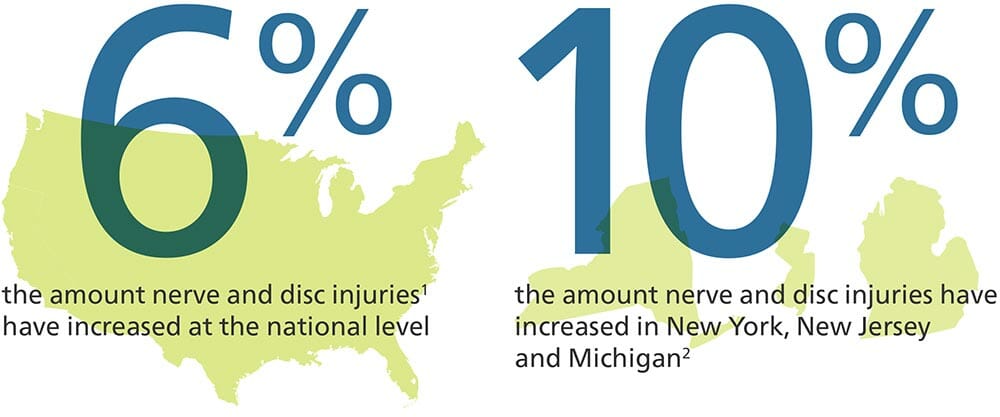

First Party Auto Casualty Nerve and Disc Injuries are on the Rise

While charge severity has remained flat in first party auto casualty—influenced, in part, by policy limits—overall severity is on the rise. This time, the culprit is an increase in nerve and disc injuries over the typically more common—and less expensive—soft tissue injuries. Certain states are seeing a higher incidence than others—in New York, New Jersey and Michigan diagnoses of nerve and disc injuries have increased by 10 percent2. At the national level, the increase is approximately 6 percent1.

Third party auto and workers’ compensation insurers should also take heed—regardless of coverage type, the introduction of a nerve and disc-related diagnosis is generally at least twice as costly as soft tissue damage.

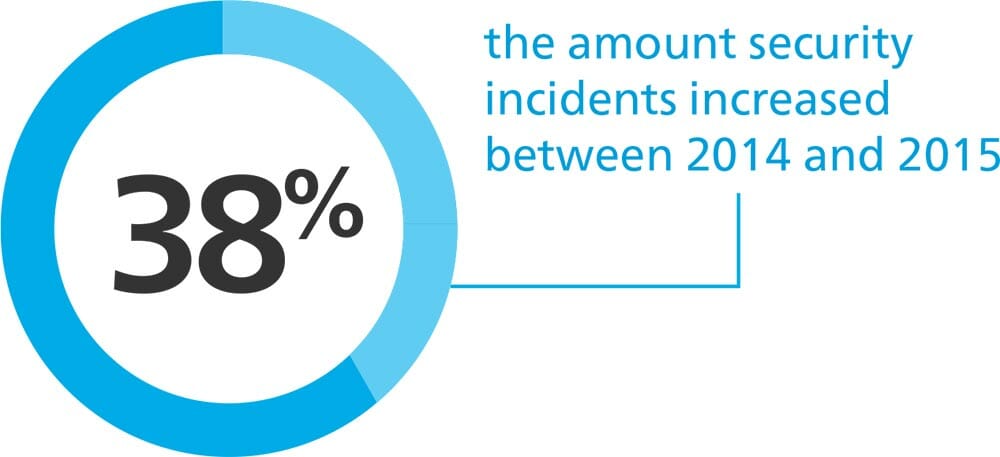

Information Security Matters More Than Ever

In 2015, there was a 38 percent increase in security incidents over 2014. And at an average cost of $1.2 million to contain an incident—out of the average $3 million security budget1—there is a lot at stake. Companies that experience a data breach have more to lose than money—reputation and customer trust are hard to win back.

So what’s a business to do? According to Verizon’s 2016 Data Breach Investigations Report, there’s no easy answer. However, two tactics that could prove to be particularly useful are web app patching and multifactor authentication. Together, these could have prevented almost half the 2015 incidents.

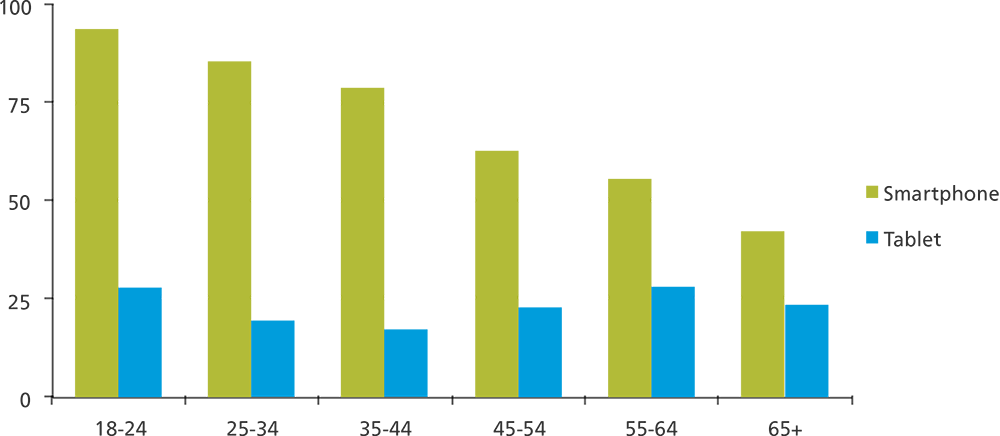

Mobile is a Must

According to comScore’s 2016 Mobile App report, “digital media time in the U.S. continues to increase — growing more than 50 percent in the past three years, with nearly 90 percent of that growth directly attributable to the mobile app.”

Hours Spent Using Mobile Apps Each Month by Age Range1

For insurance companies, mobile applications help improve customer relationships and build satisfaction in a number of ways: delivering information to prevent claims, allowing them to submit claims information like first notice of loss, and providing real-time updates of claims status. Companies like Lemonade, recently licensed in New York, and Spixii, soon to be licensed in the U.K., are even using artificial intelligence-driven chat bots to power 100 percent digital interactions with customers.

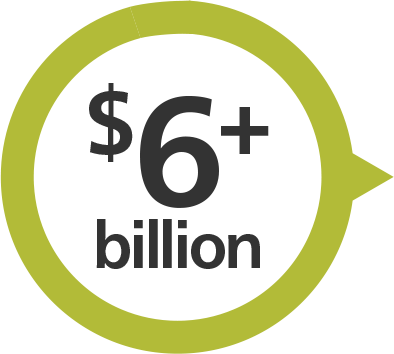

Third Party Auto Casualty and Workers’ Compensation: Charge Severity Is Rising

Charge severity is on the rise for third party auto and workers’ compensation insurers. In third party auto, average charge per claimant in 2011 was $8,285. Through the third quarter of 2016, it was $13,499—that’s a 62 percent increase1. Workers’ compensation is seeing an even more dramatic increase over 2011—a whopping 202 percent2. The third party charge severity increase is being driven by a combination of increased unit cost and utilization, while the workers’ compensation increase is primarily due to increased utilization.

Interestingly, first party auto charge severity has stayed relatively flat, influenced, in part, by policy limits.

Data is Delivering on its Promise

The insurance industry as a whole is seeing technology transformations of all types—and making use of data is at the forefront of their investments. In fact, a recent study by Strategy Meets Action indicates 82 percent of insurers are focusing on strategic projects related to data analytics. This expenditure is second only to customer experience projects.  While dashboards and reports are cornerstones of any analytics program, it’s important that access to information that informs decision making is embedded throughout claims workflows. Shahin Hatamian, Vice President of Product Management, Mitchell So how do companies go from Big Data to actionable insights? One good place to start is by understanding claims analytics personas. What a claims executive is looking for is not necessary what an adjuster needs to know. Further, where and when that information is available makes a difference—while dashboards and reports are cornerstones of any analytics program, it’s important that access to information that informs decision making is embedded throughout claims workflows.

While dashboards and reports are cornerstones of any analytics program, it’s important that access to information that informs decision making is embedded throughout claims workflows. Shahin Hatamian, Vice President of Product Management, Mitchell So how do companies go from Big Data to actionable insights? One good place to start is by understanding claims analytics personas. What a claims executive is looking for is not necessary what an adjuster needs to know. Further, where and when that information is available makes a difference—while dashboards and reports are cornerstones of any analytics program, it’s important that access to information that informs decision making is embedded throughout claims workflows.

Opioid Abuse is an Insurance Pain Point

Opioid abuse has reached epidemic proportions—in fact, every 19 minutes, someone in the U.S. dies from an opioid overdose. With $1.5 billion in opioid-related expenditures, the P&C industry has a lot at stake. Earlier this year, the CDC released their official Guideline for Prescribing Opioids for Chronic Pain that offers specific steps physicians can take to curb the problem.

There are also some actions insurers can take, including using formularies with built-in controls; putting first-fill restrictions in place; monitoring total morphine equivalent doses by patient; ensuring their PBM solution has built-in risk calculation alerts; and implementing managed care solutions.

Millennials are Driving Adoption of Usage Based Insurance

A recent Towers Watson study indicates that to succeed, insurers will need to adapt to meet the needs of the next generation of customers. In fact, in the U.S., 93 percent of millennials would buy a usage-based insurance (UBI) policy if the rates didn’t increase, while 72 percent believe it’s a better way to calculate rates. UBI presents additional opportunity with value-added services: 80 percent of millennials would pay more than $45 a month for options like theft tracking or automated emergency calls. While the trend toward UBI is just getting off the ground in the U.S.—Towers Watson anticipates 17 million people will have tried it by the end of 2016—it’s gaining ground in other countries. It’s achieved double-digit market share in Italy and markets are maturing in Germany, Spain and France.